how to get arbed with perfect information

no-arbitrage theory can be triggering

The “Bridge of Asses”

Option Pricing Explained: No Arbitrage + Financial Mathematics from a Quant | 52 min watch

Doug Costa (SIG quant, former math professor, and the teacher I learned Black-Scholes from 25 years ago) builds no-arbitrage derivatives pricing from scratch using a binomial tree. No calculus, pure replication.

The thing I want to point you to is the profound role of the no-arbitrage axiom. It is the basis of derivatives replication and, by my assertion, represents the “bridge of asses” in investing education.

As a reminder, since nobody clicks links, Wikipedia says the pons asinorum or “bridge of asses” is:

used metaphorically for a problem or challenge which acts as a test of critical thinking, referring to the “ass’ bridge’s” ability to separate capable and incapable reasoners

The notion of replication is the pons asinorum of investing education because it is:

the conceptual rails of looking at a web of branching future payoffs, seeing how they could be replicated, and measuring the cost of that replicating portfolio today. It is the formalization of finance’s deepest truth — you cannot eradicate risk, but only change its shape.

You could make an even stronger claim that it lies at the core of decision-making itself, as it formalizes opportunity cost.

And I say this without being able to appreciate its deeper impact. Doug pauses for a moment in the video to marvel: when you add no-arbitrage condition to the standard axioms of mathematics, he says, the entire field of financial engineering “blossoms” out.

His colleague frames the no-arbitrage axiom joyfully:

Either we get a formula [so we win mathematically]. Or it’s violated and we make free money. Either way, we win.

Towards the end of the video, Doug discusses reflexive pushbacks he’s encountered after teaching this.

“One piece of pushback is typically, well, maybe it’s just that with stock prices, you don’t really know the probabilities. So it’s just a matter of knowing the right probabilities— if you could really discover somehow what the true probabilities were, then it would be better to use them [than the risk neutral probabilities].”

Doug’s rebuttal shows how you would still be arbed.

“I’m going to give you an example to debunk that idea. And I call this example the coin flip contract. So I’m going to postulate that there’s a company, a corporation, that finances itself, not by selling stock, but by selling what they call coin flip contracts. And the corporation has gone to great trouble and expense to manufacture a perfect coin, meaning a coin that is exactly 50% to be heads and 50% to be tails every time it’s flipped. So the probabilities are always 1 half and 1 half guaranteed…

You can watch the video, but I paraphrased it here as well. Here’s how it works.

A company issues coin-flip contracts based on a provably fair coin. The contract pays $150 on heads, $75 on tails. These trade in a secondary market at $100. Interest rate is 0%.

So we know everything. The probabilities aren’t hidden or estimated. They’re printed on the coin: p = ½.

Now: what’s the no-arbitrage price of a 110-strike call on this contract?

p̂ = (100 − 75) / (150 − 75) = ⅓

Call value = ⅓ × $40 + ⅔ × $0 = $13.33

Delta = (40 − 0) / (150 − 75) = 8/15 of a contract

Now suppose you say: I know better. The real probabilities are ½ and ½, and I’m not going to ignore them. Expected payoff is ½ × $40 = $20. So you buy the call from me at $20.

Here’s what I do next. I’m short the call. I immediately buy 8/15 of a contract to hedge.

Heads: My 8/15 position gains 8/15 × $50 = $26.67. Plus your $20 premium, I have $46.67. I owe you $40 (I have to buy the contract at $150 and sell it to you at $110). Net: +$6.67.

Tails: My 8/15 position loses 8/15 × $25 = $13.33. But I have your $20 premium. Net: +$6.67.

Every time. Both states. Guaranteed $6.67. I haven’t predicted anything. I don’t care what the coin does.

What did you get? Heads: gain $40 on the option, paid $20, net +$20. Tails: lose your $20 premium, net −$20. You’ve turned a coin flip into a coin flip — a $20 bet where you win or lose based on what the coin does.

If you try to hedge back? Doesn’t matter how you move delta. Win more on heads, lose more on tails. Move it down: vice versa. The best you can do is lock in a guaranteed $6.67 loss.

You had perfect information about the true probability….and you still got arbed buying the calls (you should have bought the contract!).

The market-maker doesn’t need a view on the coin, just the ability to trade the underlying and the derivative simultaneously. And acquiring the knowledge to cross the “bridge of asses.”

A random personal thought:

I suspect is kind of triggering for some people. It offends one’s sensibilities to think

that understanding derivative pricing ends up trumping knowledge about the true odds of things.

It’s like you spend all this time researching and learning and at the end of the day some market-maker knows just enough to not trade at the wrong price with you anyway. I’m overstating that reality, getting picked-off is real and market-makers are rightfully paranoid. But I guess that’s why I’m drawn to replication as a way of thinking. A trader is just looking for some free money when your bid or offer presents a contradiction. And that hunt makes all prices a little smarter, which, is a public good (but also a frustrating result for traders themselves, which is why the job is always uphill. A byproduct of your success is a smaller TAM).

Just to be thorough, this replication thing applies mostly to derivatives. The arb needs to be able to trade the derivative and the underlying and all advantage comes from the relationship between the two. The arb is useless without relative value.

Related learning:

Understanding Risk-Neutral Probability | Moontower

Moontower Presentation on Black Scholes “As a Trading Strategy” | Slides

- The slides for that presentation are based on this post: The Intuition Behind The Black-Scholes Equation

[UPDATED]

As I expected, the post how to get arbed with perfect info would trip people up. I didn’t expect confusion because I thought Professor Doug Costa, whose explanation is featured in that post, was itself confusing. But because the concept of replication is hard and feels like it violates the good. It’s triggering. It means you can know the truth and still get arbed. Again, this is why I call it the pons asinorum of finance.

A reader brought it up in our Discord so I’m going to share the discussion here as he felt like our back and forth helped.

Before getting to the conversation, let’s refresh the problem Doug set up:

A company issues contracts based on a provably fair coin. The contract pays $150 on heads, $75 on tails. It trades at $100. Interest rate is 0%.

You calculate the true expected value of the 110 call using the true probability of 50%.

It’s worth $20 because it has a 50% chance of being $40 in-the-money.

You pay $20 for it (but even if you paid a bit less for an unambiguously positive EV trade, this analysis will hold. I just want to stay with Professor’s example)

The dealer sells it to you, hedges with 8/15 of the underlying contract, and locks in $6.67 profit in both states. Pure arb.

You had perfect information about the true probability and you still got arbed. The dealer made money in all scenarios, trading the call at fair value with you.

Doug is showing how the real-world probability doesn’t matter to the derivatives trader if they can also trade the underlying. In this case, the underlying is mispriced, but the dealer doesn’t know that. All the dealer cares about is whether the relationship between the derivative price and the underlying price is mispriced. In this contrived example, the mispricing was more profitable than knowing the true probabilities.

And to add something Doug doesn’t mention…if the investor knew the stock was underpriced and bought that instead, they’d have a positive EV trade (the fair price of the stock is $112.50) but they are still worse off than the dealer who knows the relative value of the 2 securities is wrong and gets to make a profit in all scenarios.

This is a good place to insert the chat.

Reader: I see, so the main point is we can converge a spread by trading two things instead of betting on one.

Kris: In a world with no derivatives, you’re left with having to be good at guessing real-world probabilities, but derivatives are their own source of possible edge that doesn’t inherit from knowledge of the future but from relative mispricings between the derivative and the underlying.

It’s obvious that being able to handicap probabilities would be a source of edge, but it’s quite subtle that once you introduce derivatives and the idea of replication, there becomes a source of profit that doesn’t rely on such an ability.

Reader: Right, so it’s instructive in giving one more spread to look at. If you used a put in your example, then the dealer would lose because they’d be too short. Then a dealer that actually has no information and sells both sides ends up $0. This example is picking the (long) side where it wins.

Kris: Yeah, the underlying in this example is too cheap RELATIVE to the call option.

If the call option was $13.33, then from the vantage point of real-world probability, both the underlying and call are too cheap, but they are priced correctly with respect to each other.

Which makes the point — if a derivative and underlying are correctly priced to each other, then the real-world probability is not important to the dealer. The dealer only cares about the relative values.

You can just compute the Sharpe of buying one vs the other I suppose to see which is better (that’s one lens). The call is more underpriced in % terms, 3.33 when it’s worth 20. But it’s more volatile as it will lose all of its value when it loses.

I’d just stick them both in a Kelly calculator in Claude or something and whichever one it says bet more on is the better one lol.

There are some important implications here. And brain damage — investor brain and derivatives brain collision.

The goal is that derivativesbrainskill.md becomes something one calls as needed, like Neo downloading kung fu. But you don’t wanna get carried away with it and shoot it at everything in life. It’s this weird artificial thing that works in a replication context, but it’s also not artificial in that its violation presents hard cash arbitrage!

That’s the end of the chat, but let me add one more thing to make you feel better if it’s still foggy.

I’ve seen this subtlety trip up seasoned options traders where they take B-S pricing to mean that the forward for a stock is stock grown at the risk-free rate (RFR), but this is ONLY true in a world where you can trade the underlying AND the options. Outside the context of replication, you cannot make that assumption.

Struggling with this idea is entirely forgivable. I mean, the realization that you could use RFR as the discount rate was a revolutionary breakthrough. Bachelier figured out option pricing in the early 1900s, but he and his contemporaries were stumped by what rate to discount the payoffs.

Later academics wondered if you should use something like the required return from CAPM or something, but it was the whole idea that if you trade a derivative vs the underlying against one another, then you can have equivalent payoffs and therefore it’s riskless to go long one and short the other. If it’s riskless, then RFR is the appropriate discount rate.

Warren Buffett sees the necessity of agnostic dealers using the RFR to price options in arbitrage-free ways as an opportunity. He asserts that put options are overpriced because they use too low of a discount rate, but the dealers don’t care so long as they can trade the underlying, they can arb any other rate assumption. Again, so long as “they can trade the underlying.”

This single idea allows derivatives traders who know nothing about the fundamentals of securities to make money in a sea of people who do. It’s quite profound and not a small part behind why I think vol trading is easier than directional trading.

A final follow-up

A reader asked:

How did I get to the 8/15 hedge ratio?

It came from Prof Costa’s setup:

A stock is 50/50 to go to $150 (up) or $75 (down) from $100. What is the no-arbitrage price of a 110-strike call on a one-period binomial?

p̂ = (100 − 75) / (150 − 75) = 1/3

Call value = 1/3 × $40 + 2/3 × $0 = $13.33

Delta = (40 − 0) / (150 − 75) = 8/15 of a contract

Let’s take this apart.

Risk-neutral probability of stock going up

p̂ is the risk-neutral probability of the stock going up.

How do we get that intuitively?

Start with the payoffs:

- Up_payoff = 1.5x

- Dn_payoff = .75x

The risk-neutral probability is the one that makes the stock price fairly priced given the possible payoffs. In other words, if you buy the stock, the expected return is 0. It must satisfy this equation:

p̂ (Up_payoff) - (1-p̂ ) (Dn_payoff) = 0

Solve for p̂:

p̂ (Up_payoff) - Dn_payoff + p̂(Dn_payoff) = 0

p̂ (Up_payoff + Dn_payoff) = Dn_payoff

p̂ = Dn_payoff / (Up_payoff + Dn_payoff)

Concisely stated:

p̂ = d/(u + d)

p̂ = .75/(1.5+.75)

p̂ = 1/3

When in doubt, you can always set up the expected value equation and solve the algebra. You don’t have to memorize a formula.

But you can also put on your gambler goggles.

If something pays 2-1 odds like a money line of +200 or a prediction market trading at 33, then the implied risk-neutral probability is 1/3.

If you buy this stock, you risk $25 to make $50.

Just remember the intuitive odds to probability converter:

x-to-y odds = y / (x + y) probability

2 to 1 odds = 1/(2+1) = 1/3

This is just symbols for “If I get paid 2-1 when I win, then I must win 1 out of 3 times for this to be fair”

You can practice some more in these posts:

- the arbitrage reflex is more profitable than the opinion reflex

- Binary Straddle Example Based On The 2016 Election

The hedge ratio

Back to the original example…if you’re short one call, you buy 8/15 of a share to be delta-neutral. The numerator is the spread in the call’s payoff across the two states ($40 vs $0). The denominator is the spread in the stock’s payoff ($150 vs $75).

Delta is just option change over stock change. How much the derivative moves for a move in the underlying.

The formula in terms of return:

delta = (C_up - C-down) / S (Up_payoff - Dn_payoff)

delta of the 110 call= (40 - 0) / 100(1.5-.75) = 40/75 = 8/15 = .533

Relative value

To reinforce the main point of Prof Costa’s talk, risk-neutral probabilities are enough to make money if you can find an inconsistency between option prices and the underlying. The real-world probability doesn’t matter in a relative framework.

By understanding the distribution of the stock, we were able to compute a delta for any contract. That distribution implies some probability embedded in the underlying. This is not the same as the real-world probability, which is decreed to be 50/50.

Professor Costa showed that if you buy the stock which was underpriced (although you didn’t know that because you computed it must be fair with a 1/3 probability of going up) as a hedge on the call delta, then if someone paid anymore than the risk-neutral fair value of the call, even if they paid less than what the real-world implied probability price is, the dealer makes free money!

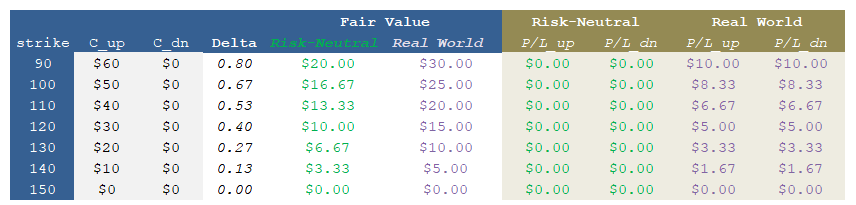

Work through the logic for a bunch of strikes and this is what you get if you sell the calls at the risk-neutral fair value (green) or real-world fair value (purple).

The dealer always wins against the real-world probability!

It is also true that the call buyer who pays some price between risk-neutral and real-world has positive expectancy but they don’t have an arbitrage.

So who loses?

The people selling the stock at $100 when the real-world probability is that it’s 50/50 to be 150 or 75. The stock should be $112.50.

Learn more:

🔗 Kellogg lecture notes that walks through exactly this kind of binomial pricing and hedging