asian options

average price options

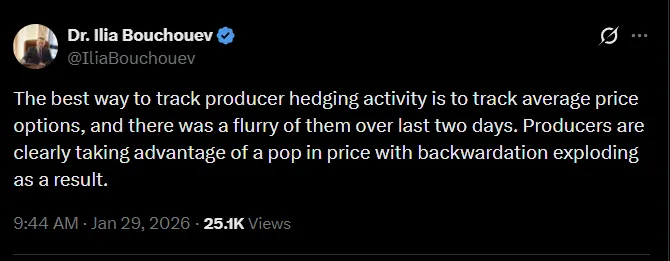

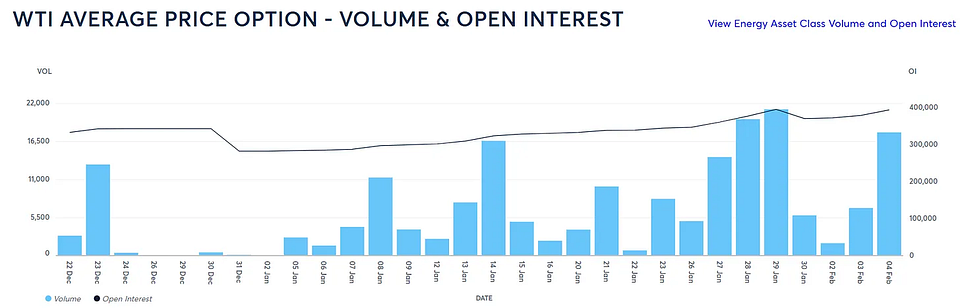

One of the traders in our Discord was discussing exotic options in commodities markets. The topic of APOs or “average price options” came up because of this tweet:

This is spot on.

From CME:

To understand why producers like APOs (also known as “Asian” options*) we should first understand what they are.

*Via wikipedia:

In the 1980s Mark Standish was with the London-based Bankers Trust working on fixed income derivatives and proprietary arbitrage trading. David Spaughton worked as a systems analyst in the financial markets with Bankers Trust since 1984 when the Bank of England first gave licenses for banks to do foreign exchange options in the London market. In 1987 Standish and Spaughton were in Tokyo on business when “they developed the first commercially used pricing formula for options linked to the average price of crude oil.” They called this exotic option the Asian option because they were in Asia.

An APO’s payoff depends on the average price of the underlying asset over a specified period, rather than just the spot price at expiration.

For example, an APO call option pays max(Average Underlying Price — Strike, 0) while an APO put pays max(Strike — Average Underlying Price, 0)

Asian options are particularly popular in crude oil for a few reasons.

- Cash flow matching: Oil producers and consumers often transact at monthly average prices, making Asian options a natural hedge

- Reduced manipulation risk: Averaging prices over time makes it harder to manipulate the settlement price

- Lower cost: The averaging mechanism reduces volatility, making Asian options cheaper than standard European options with the same strike. An appealing feature in a cost-focused commercial business with tight margins.

Poking around online, this topical information about APOs isn’t hard to find, but understanding #2 and #3 is harder to see, so let’s touch on the actual mechanics of APOs with an example.

Suppose the price of WTI is $75 and it’s January 31. You buy the Feb 75 Asian-style put.

The put payoff will be $75 — (average settlement price of WTI of the prompt future in the month of February)"average settlement price of WTI of the prompt future in the month of February"

💡average settlement price of WTI of the prompt future in the month of February

Unless you have traded Asian options you wouldn't know how this is even computed. We'll use Feb 2026 as an example.The prompt future is the March 2026 contract until its last trading date on February 20. Then the April 2026 contract is prompt. Taking account of weekends and President's Day, the March contract is prompt for 14 business days and the April contract is prompt for 5 business days. February average price = average of 14 March futures datapoints and 5 April futures datapoints.💡

Notice that each trading day in February contributes 1/19th of the final settlement price. On the last day before expiration, we have a running tally of the final settlement price — the average of the past 18 days’ closing prices. The last day’s price change is weighted by 1/19 to determine the final average for February.

This means that as you approach expiry, the gamma of this option is actually declining! You’ve already seen most of the flop, right? If the average going into the last trading day is $76, you’d need the futures to fall more than $19 on the last day for the 75 put to go in-the-money.

This explains why Asian options are less prone to manipulation and their deltas less sensitive to changes in the futures. It’s hard for the futures to move enough to materially change the average because each day gets a small weight in the calculation. This stands in stark contrast to vanilla options which have extremely high gamma near expiration. A mere 2-cent move through the strike just before expiry can be the difference between the option being 100 delta or 0 delta.

In this February option example, we are already in the “averaging period”. But what if you buy the December Asian-style 75 put on January 31? The averaging period, the calendar month of December, doesn’t start until 10 months have elapsed.

The pricing model will treat the option just like a vanilla option for 10 months, then account for how the last month’s gamma and theta shrink as each day in the averaging period contributes to the final settlement price. Your optionality is declining in that final month. Asian options have cheaper premiums than their vanilla counterparts because they act the same for some period of time, but then lose optionality relative to the vanillas in the averaging period.

In practice, a hedger may buy a “strip” of Asian options. For example, the Cal27 75 put refers to the “75 put Asian style for each month in the calendar year of 2027”. If the hedger buys 100 strips, they have bought 1200 options (100 options in each month). If a bank sells this strip to the hedger, typically in a bilateral OTC form, they could lay off the risk by buying this APO strip from market-makers. While these don’t trade on a centralized order book, the trades can be submitted to CME’s Clearport where the exchange acts as a clearinghouse and margining agent to both sides, removing counterparty risk to the street.

The bank desk does wear a trader hat in the act of facilitating this flow. They aren’t required to “back-to-back” the risk or cover it exactly as they opened it. For example, if the bank thought the vols in the second half of 2027 were expensive, they could just buy options covering the first half of the year effectively legging a short forward vol term structure trade. If they thought put skew was expensive, they could buy a call strip instead of covering the puts. This would neutralize their vega, but leg them into a short skew risk reversal. They could weight their own hedge in a way to express their bias. They could trade plain American or European options if they thought they’d get tighter prices from a wider pool of traders (more traders deal in vanillas then Asian style options) and sweat the Asian vs vanilla mismatch. The menu of possibilities highlights how valuable it is to have deal flow. You know you are getting to sell on the offer on one side of the deal and then you can try to trade mid or better when covering some or all of the risk. Commodity option trading is a fun global boardgame!

I’ll wrap up with this blurb from my friend Mat. I found it interesting because I have sometimes thought that it’s a historical accident that the most popular options are American-style vanillas when you can see how cash-settled European or even Asian-style options would make more sense.